Which brands stood out in 2Q25?

Apple has been highlighted in the IDC report with the iPhone 16 being the highest-shipped model across India in the first half of 2025, making up 4 per cent of the overall shipments. Apple also continued to maintain its growth with shipments growing 21.5 per cent YoY to 5.9 million units in the same period.

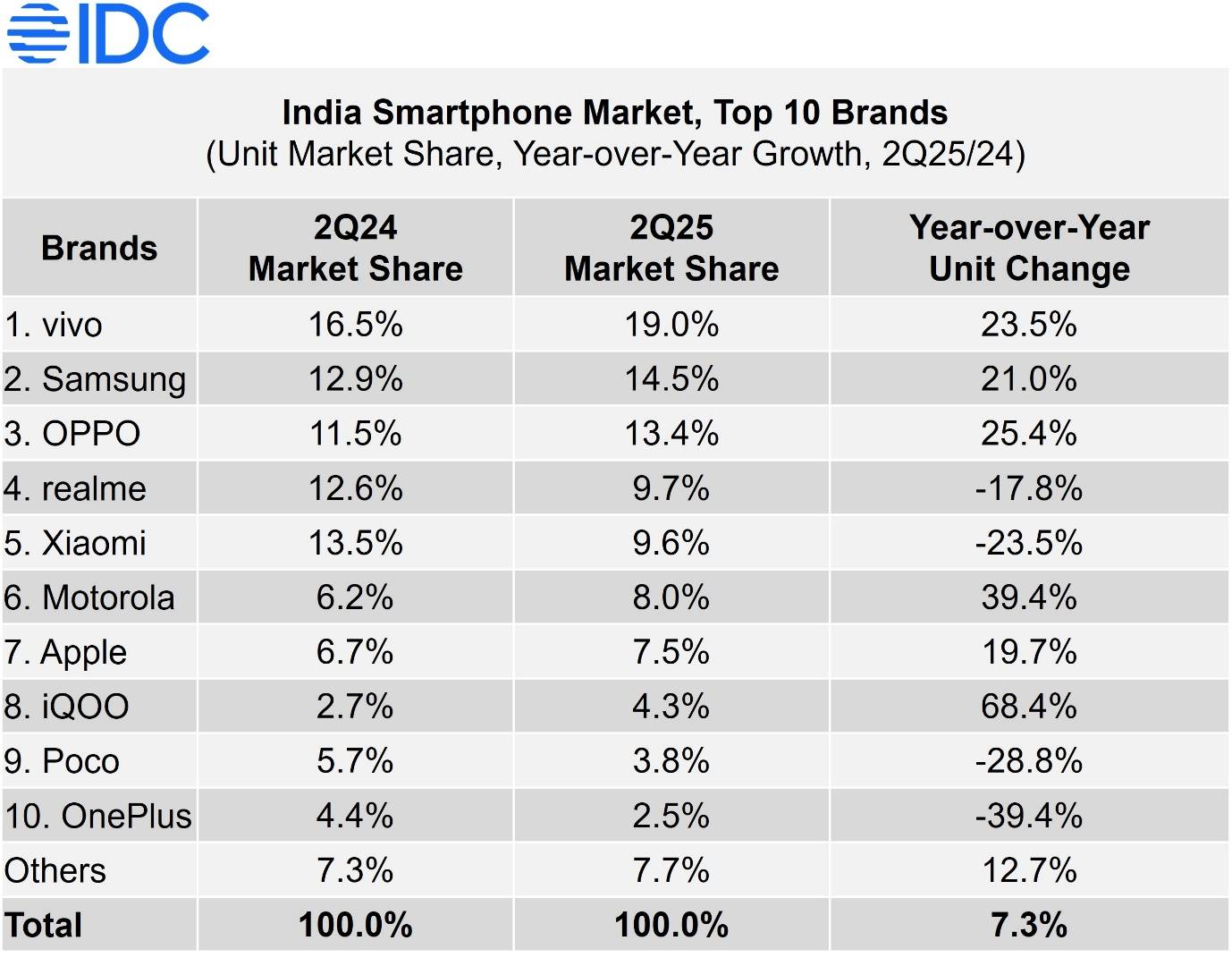

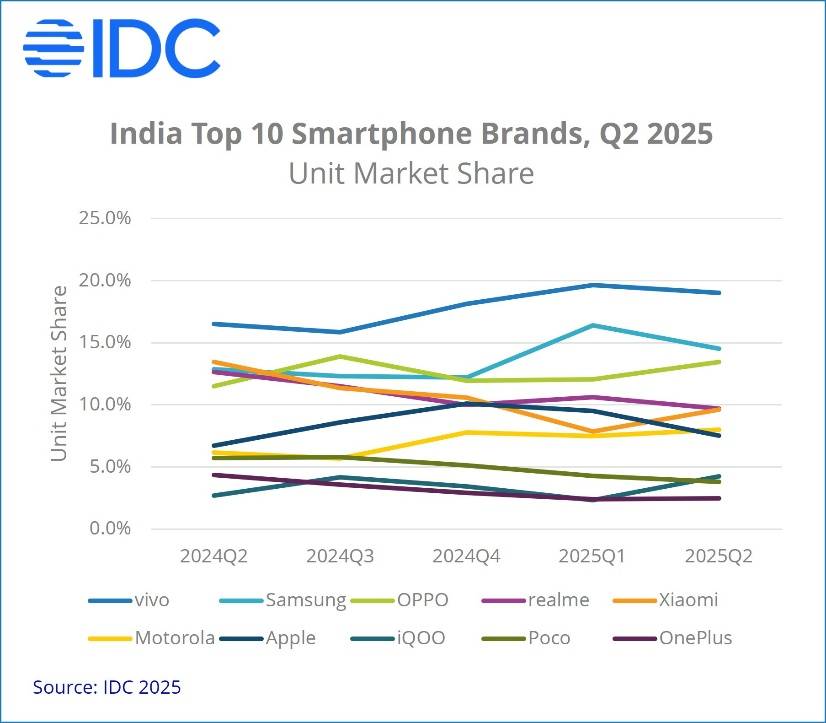

Vivo led India’s smartphone market for the sixth straight quarter with a 19.0 per cent share in H1 2025, up from 16.5 per cent a year ago, driven by a balanced portfolio across segments and channels. Samsung ranked second with 21.0 per cent growth, boosted by five new Galaxy A/M/F series launches, bringing Galaxy AI and long-term updates to the mid-range. OPPO held third place with a 13.4 per cent share, aided by the K13, A5x, and strengthened service support.

Two brands that stood out for the highest YoY growth were Nothing with 84.9 per cent, followed by iQOO with 68.4 per cent.Nothing Phone (3a) and Phone (3a) Pro were launched in March, while iQOO updated its mid-range lineup with the Neo 10R and Neo 10.

Premium and mid-range segments drive Q2 growth as budget share dips

In Q2 2025, entry-level phones (below Rs 8,300) grew 22.9 per cent YoY to a 16 per cent share, led by Xiaomi’s Redmi A4 and A5. The Rs 8,300–Rs 16,600 segment rose 1.1 per cent but slipped to 42 per cent share, dominated by Vivo, OPPO, and Realme. Entry-premium models (Rs 16,000–Rs 33,000) fell to a 27 per cent share on a 2.5 per cent drop, with Vivo, Samsung, and OPPO leading, while Motorola climbed to fourth.

Mid-premium (Rs 33,200–Rs 49,800) grew 39.5 percent to 5 percent share, driven by OPPO and OnePlus. Premium (Rs 49,800–Rs 66,400) surged 96.4 per cent, doubling share to 4 per cent, with iPhone 16 and iPhone 15 making up over 60 per cent of shipments. Super-premium (above Rs 66,400) grew 15.8 per cent, steady at 7 per cent share, as Samsung edged past Apple, 49 per cent to 48 per cent.

MediaTek-based shipments led with a 44.3 per cent share, though this is down from 56.1 per cent on a 15.4 per cent decline, while Qualcomm-based phones grew 37.6 per cent YoY to reach a 33.9 per cent share.

Interestingly, offline channel shipments grew 14.3 per cent with share rising to 53.6 per cent, as online shipments remained flat and share dipped year-on-year to 46.4 per cent. Offline growth is said to have been fuelled by strategies such as higher channel margins, in-store promoters, and price cuts, while e-tailers countered with summer sales offering steep discounts on mid-range and premium models.

IDC says the smartphone market has recovered from a two-quarter slump, but annual growth may remain weak due to soft demand and rising prices. Shipments in 2025 are expected to see a low single-digit decline, with budget demand hit by macroeconomic challenges. For the second half of the year, IDC advises brands to push fresh shipments instead of relying on heavy promotions to clear old stock.

Conclusion

India’s smartphone market is showing cautious recovery in H1 2025, with mid-premium and premium segments driving growth while budget and entry-premium categories see slower momentum. Vivo’s continued leadership reflects a strong multi-segment strategy, Samsung’s Galaxy AI integration and long-term updates are paying off in the mid-range, and emerging brands like Nothing and iQOO are carving out niches with aggressive launches.

For buyers, this means more choice and better value across price brackets. Premium users will find iPhone 16 and 15 widely available, while mid-premium shoppers can explore OnePlus, OPPO, and Vivo models benefiting from robust offline availability and attractive offers. Budget-conscious consumers may still find deals on Xiaomi, Realme, and entry-level Vivo phones, but rising prices and macroeconomic pressures suggest making purchases sooner rather than later.

Overall, the market trends indicate a shift toward higher-value devices and offline sales growth, signaling that brands prioritising innovation, availability, and real-world usability are best positioned to win in India’s evolving smartphone landscape.

OPPO K13 Turbo, K13 Turbo Pro debut as brand's first gaming-centric phones in India

Infinix GT 30 5G+ launches in India with MediaTek Dimensity 7400, 5,500mAh battery, and dedicated gaming features

Vivo Y400 5G launched in India with 6,000mAh battery, AMOLED display, and rugged build

")

")

")